High and rising government debt slows growth, crowds out private investment, limits the government’s ability to respond to unexpected emergencies, and elevates the risk of a sudden fiscal crisis, where investors would lose confidence in U.S. Treasury bonds and the U.S. dollar. This fact sheet lays out everything legislators and the public need to know about the U.S. federal debt to help them examine the unsustainability of the U.S. budget.

The total or gross federal debt is $31.5 trillion. This is the debt subject to the debt limit.

At 120 percent of gross domestic product (GDP), the gross federal debt exceeds the amount of goods and services produced in the United States every year by one‐fifth.

The total federal debt burden per U.S. person is $94,000.

The total federal debt burden per U.S. household is $240,000.

Total federal debt consists of publicly held debt (borrowed from credit markets, including from individuals, state/local governments, foreign entities, and the Federal Reserve) and intragovernmental debt (borrowed from federal trust funds like Social Security).

The publicly held or public debt is $24.6 trillion. This debt is borrowed in credit markets.

At 95 percent of gross domestic product, the publicly held debt is approaching the size of the U.S. economy, as measured by all the goods and services produced in the United States in one year.

Such high levels of debt reduce economic growth. Researchers identified that government debt drags down economic growth beginning at 78 percent of GDP.

Economists focus on the publicly held debt to assess how government debt affects interest rates and crowding out of private investment, because this debt is mostly held outside the federal government and traded in public markets.

The public debt will surpass its WWII‐high of 106 percent of GDP by 2028.

The public debt is projected to grow to 118 percent of GDP by 2032 under CBO’s optimistic scenario and to 130 percent of GDP by 2032 under a more realistic scenario, in which the 2017 middle class tax cuts are extended.

We owe one‐third of the publicly held debt to foreign entities; two of our biggest foreign bondholders are China and Japan.

The U.S. Federal Reserve holds about one‐quarter of publicly held debt. When the Fed buys U.S. government debt, this is called quantitative easing, and represents the issuance of new money in the economy. When the money supply increases faster than production, this leads to inflation.

The federal government paid $475 billion in interest costs in 2022. Net interest is the cost of servicing the publicly held debt, paid to foreign and domestic bondholders.

10 cents of every taxpayer dollar the federal government collected last year went toward paying the interest on the debt.

If average annual interest rates were 1 percentage point higher than CBO projects, cumulative interest costs would increase by $4 trillion over 10 years.

The annual federal deficit will more than double over the next 10 years from $1.4 trillion in 2023 to $2.9 trillion in 2033. The annual deficit is the difference between annual government spending and revenues.

Federal spending is projected to rise to 25 percent of GDP by 2033. That’s 4.4 percentage points above the historical average over the last 50 years.

Federal revenues will rise to 18 percent of GDP, about 1 percentage point above the historical average.

The 75‐year unfunded obligation, as reported in the Financial Report of the United States Government, is $79.5 trillion. That’s the difference between the present value of total government receipts and total non‐interest government spending over the next 75 years.

95 percent of the total non‐interest unfunded obligation is driven by social insurance programs (98 percent by Social Security and Medicare; and less than 0.2 percent by Railroad Retirement and Black Lung Benefits).

Public debt will reach 200 percent of GDP by 2046 and 566 percent of GDP by 2097.

According to Treasury and the Office of Management and Budget: “the continuous rise of the debt‐to‐GDP ratio indicates that current fiscal policy is unsustainable.”

Further reading:

The Debt Limit and the High Costs of Debt [Cato]. “High and rising debt slows growth, crowds out private investment, limits the government’s ability to respond to unforeseen emergencies, and elevates the risk of a sudden fiscal crisis where investors would lose confidence in U.S. Treasury bonds and the U.S. dollar.”

The CBO Budget and Economic Outlook in the Post‐COVID Fiscal Era [Cato]. “CBO forecasts a worsening fiscal trajectory characterized by high and rising federal debt [in which] pandemic spending followed by a surge in interest costs [has] accelerated the [unsustainability of the U.S. budget.”

The Impact of Public Debt on Economic Growth [Cato]. Academic research has identified a negative effect of high and rising debt levels on economic growth. “For the 25 studies that provide threshold estimates, [the] mean and median threshold levels [where debt drags down growth] are found at 78 percent and 82 percent of GDP [for advanced countries], respectively.”

Q&A: Gross Debt Versus Debt Held by the Public [CRFB]. “This explainer will lay out everything you need to know about the different measures of debt and what they mean for the government’s fiscal situation.”

Download a printable PDF version of this fact sheet here.

In yet another sign that the universe loves freedom, my latest Forbes column on the Silicon Valley Bank mess was published on the same day as Saule Omarova’s New York Timesop‐ed. My column makes the opposite case as Omarova, which I’ll get to in just a bit. It also points out something that seems to be getting lost during these debates over whether to increase the FDIC insurance cap to more than $250,000: Omarova and her fellow travelers want the full provisioning of money by the government.

Further, they want to “clarify banks’ place in U.S. society and their relation to the government,” such that all money becomes “a governmental product.” They actively hail a “new monetary era” with central bank digital currencies, a digital version of the dollar that ties citizens directly to the government. They want to transform the Fed into a provider of first resort instead of a lender of last resort.

In the New York Times, Omarova glosses over this issue and claims her nomination to lead the Office of the Comptroller was sunk because of her views on deregulation. Here’s the full paragraph:

The banking industry and its political allies waged a highly public campaign to block my candidacy and called my academic work, which examined the many failings of our financial system and called for stronger public oversight, “un‐American.” But what ultimately sunk my chances was the fact that I openly opposed loosening regulatory restrictions on America’s banks.

Perhaps someone did view her work calling for stronger public oversight as un‐American. But the real controversy was her work calling for “the complete migration of demand deposit accounts [at commercial banks] to the Fed’s balance sheet.” It didn’t help when she pointed out that the “compositional overhaul of the Fed’s balance sheet would fundamentally alter the operations and systemic footprints of private banks, funds, derivatives dealers, and other financial institutions and markets.”

It’s pretty convenient to leave out the complete overhaul of private financial markets and focus on looser regulatory restrictions.

Speaking of looser regulations, I’ve noted in Forbes (multiple times) and Cato at Liberty that the Economic Growth Act of 2018 didn’t really roll back much. The only thing it did was make a symbolic change to the threshold for enhanced supervision, from $50 billion to $250 billion. But the Fed maintained all the discretion they needed to regulate banks in the range from $100 billion to $250 billion more stringently if they thought it was necessary, and it’s not as if federal regulators couldn’t place activity restrictions on banks with less than $100 billion in assets.

Whether the 2018 changes had anything to do with Silicon Valley Bank’s failure is an open question, but it’s very difficult to make that case. Among other issues, it turns out the 2014 rules for one of the so‐called enhanced regulations, the liquidity coverage ratio, used a higher threshold of $250 billion from the very beginning (with a modified ratio at a lower threshold). Similarly, the 2014 rules for the Fed’s Comprehensive Capital Analysis and Review (CCAR), a close companion to the Dodd‐Frank stress tests, another of the so‐called enhanced regulations, also used the $250 threshold.

The threshold could have been lower, but the consensus leading up to the 2018 bill—Democrats on the Senate Banking Committee could have stopped the whole thing—was that the added regulations were redundant. And in the case of Silicon Valley Bank, at least through 2022, it had just as much equity and liquidity (if notmore) than even the largest, most stringently regulated large banks.

Regardless, the threshold was always arbitrary. There was no objective reason to argue that a $50 billion bank was systemically important and a $25 billion bank (or two of them) wasn’t. In hindsight, it’s easy to argue the threshold should have been lower, especially after the government scared the daylights out of everyone by invoking emergency authority and making even uninsured depositors whole.

Of course, Omarova wants to undo the 2018 changes. But that’s not enough. What she really wants now is to have the federal government take a special “golden share” interest in “each individual bank above a certain size.” According to Omarova:

It would be structured to serve a single purpose: to give the American public a seat at the table where banks make decisions on how to manage—or perhaps not manage—the risks we ultimately may have to bear.

The “golden share” would also “allow the federal government to place one director on the bank’s board.” And while Omarova acknowledges that “This model may seem like government takeover to some,” she’s careful to point out “that’s not how it is designed to work.” Just in case, though, the “beauty of the golden share” is that it “can be tailored to serve any public goal.” (Ignore who gets to decide what the public goal might be.)

I won’t quibble over whether the golden share is government ownership. Either way, this idea puts too much faith in any individual to be able to recognize those “credible reasons to worry about the bank heading down a dangerous path” with, for example, “rapid growth in the riskiness or concentration of the bank’s assets or liabilities.”

The mechanism Omarova envisions is just another version of what we already have. Instead of a Federal Reserve or FDIC employee trying to stop things before they get out of hand, this person will be a federal official on the private bank board. Or maybe a Fed employee on the bank board? Either way, if it doesn’t work, the government could just take two seats on the board. That would be bulletproof.

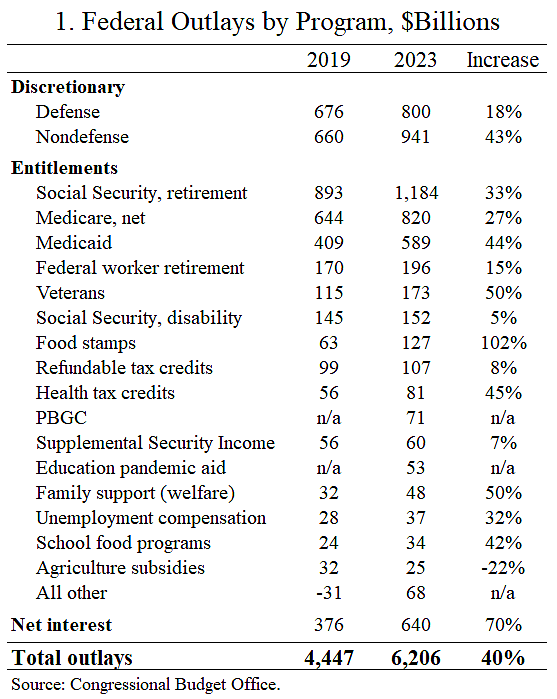

Federal spending jumped from $4.45 trillion in 2019 to $6.21 trillion in 2023, according to the Congressional Budget Office. That is a 40 percent increase in four years. The pandemic supercharged the federal budget, and spending and deficits are expected to continue rising unless policymakers pursue major reforms.

What is all the new spending since 2019? The answer is surprising, as shown in the two tables below. The main drivers of the recent increases have not been the largest three programs—Social Security, Medicare, and defense—but rather rapid growth in numerous other programs.

Table 1 shows CBO spending for 2019 and baseline estimates for 2023. The largest increases have been nondefense discretionary, Medicaid, veterans, food stamps, health tax credits, welfare, school food programs, and interest. All data in both tables are fiscal year outlays.

Some of the 2023 spending is temporary and should decline in coming years, such as the PBGC aid and education pandemic aid. Nonetheless, CBO projects baseline spending to rise at an annual average rate of 4.8 percent over the coming decade. The projections show that Social Security, Medicare, and Medicaid will be the main growth drivers ahead, but the past four years show that other programs will also grow rapidly if not controlled.

What about Ukraine? CRFB tallies the total authorized (but not necessarily spent) funding so far as $67 billion for defense aid and $46 billion for nondefense aid. If I am reading CBO correctly, they estimate that about $36 billion of the defense aid will be spent this fiscal year.

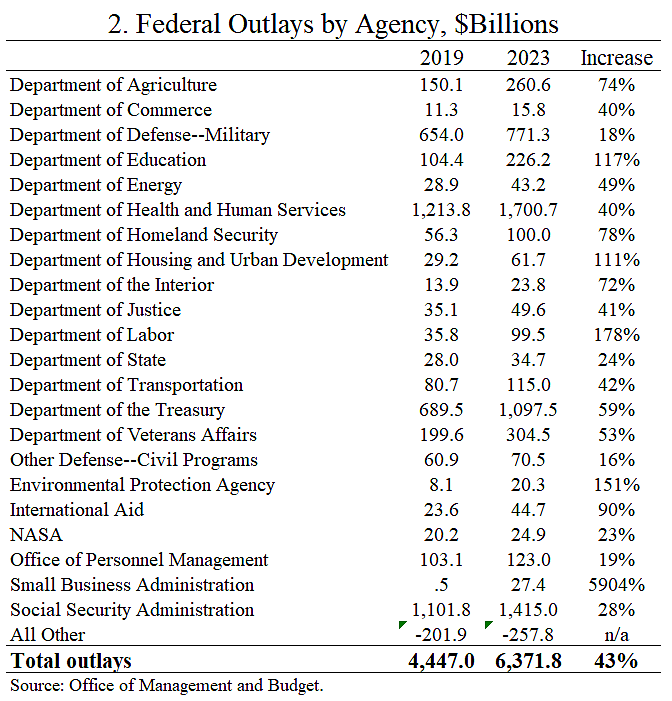

Table 2 shows spending data from President Biden’s recent budget broken out by major agency. The budget puts the increase between 2019 and 2023 at 43 percent, and Biden is proposing an 8 percent increase for 2024. The data are from Table 4.1 here.

What programs are behind the largest increases in the table? Agriculture: food stamps. Education: college aid and pandemic school aid. HUD: numerous programs. Labor: PBGC aid to troubled pension plans. Treasury: interest costs. EPA: state grants. International Aid: Ukraine. SBA: disaster loans.

Republicans led the way on spending increases in 2020, and then handed the big government baton to the Democrats for 2021 and 2022. Now some Republicans want to reverse course and leverage the upcoming debt limit debate to start cutting. What should they target?

How about a “last in first out” strategy? Reformers could push for cuts to the programs that have grown the most since 2019. Medicaid, food stamps, education aid, housing programs, welfare, the EPA, and international aid would all be good targets to downsize.

By the way, outlays from 2019 to 2023 are up 47 percent for the operations of the legislative branch and 58 percent for the Executive Office of the President. How about these institutions showing some budget leadership and cutting their own costs?

Recent commentary on federal spending is here and here, and further proposals to cut spending are here,here, and here.

Data Note. The “all other” row in Table 2 is the net of other spending programs and hundreds of billions in offset receipts, which are explained here.